- Login

- Search

- Contact Us

-

Have a question? Our team is here to help guide you on your automation journey.

-

Explore support plans designed to match your business requirements.

-

How can we help you?

-

English

Close

- Resources

Featured

Named a 2026 Gartner® Magic Quadrant™ Leader for RPA.Recognized as a Leader for the Eighth Year in a Row Download report Download report

Named a 2026 Gartner® Magic Quadrant™ Leader for RPA.Recognized as a Leader for the Eighth Year in a Row Download report Download report

- What is the role of AI in the lending industry?

- Key components of AI in lending: The modern agentic stack

- Key benefits of AI-powered lending

- The industry-wide impact of AI in lending

- AI lending and customer experience

- AI lending for enterprises (commercial lending)

- The future of AI in lending: Toward 2030 autonomous finance

- Overcoming hurdles in AI implementation

- Conclusion: Winning with an AI-first lending strategy

- FAQ: Navigating AI-powered lending in 2026

- How does AI in lending impact the accuracy of credit risk?

- How can banks ensure regulatory compliance when they adopt AI?

- What is the impact of AI on the lending lifecycle?

- What are the first steps for financial institutions starting an AI implementation?

- How does commercial lending benefit from artificial intelligence compared to consumer?

What is the role of AI in the lending industry?

AI in lending is no longer just about chatbots; it is the application of machine learning and artificial intelligence (AI) agents across the entire credit lifecycle. This includes everything from document ingestion and credit risk scoring through decisioning, compliance logging, and capital deployment.

Most financial institutions have now run at least one AI pilot. The question in 2026 is why so few have moved beyond the demo environment to enterprise-scale production. The banking sector is currently facing an operational divide between "suggestion" (copilots) and "execution" (agents).

True operational efficiency requires an execution layer that connects to the legacy infrastructure where lending actually runs. Agentic process automation (APA) provides the governance layer required for AI in lending to move from pilot to production. coordinating machine learning models, RPA bots, and human judgment.

The financial institutions building agentic banking infrastructure now are establishing a cost and capability advantage that compounds as adoption accelerates.

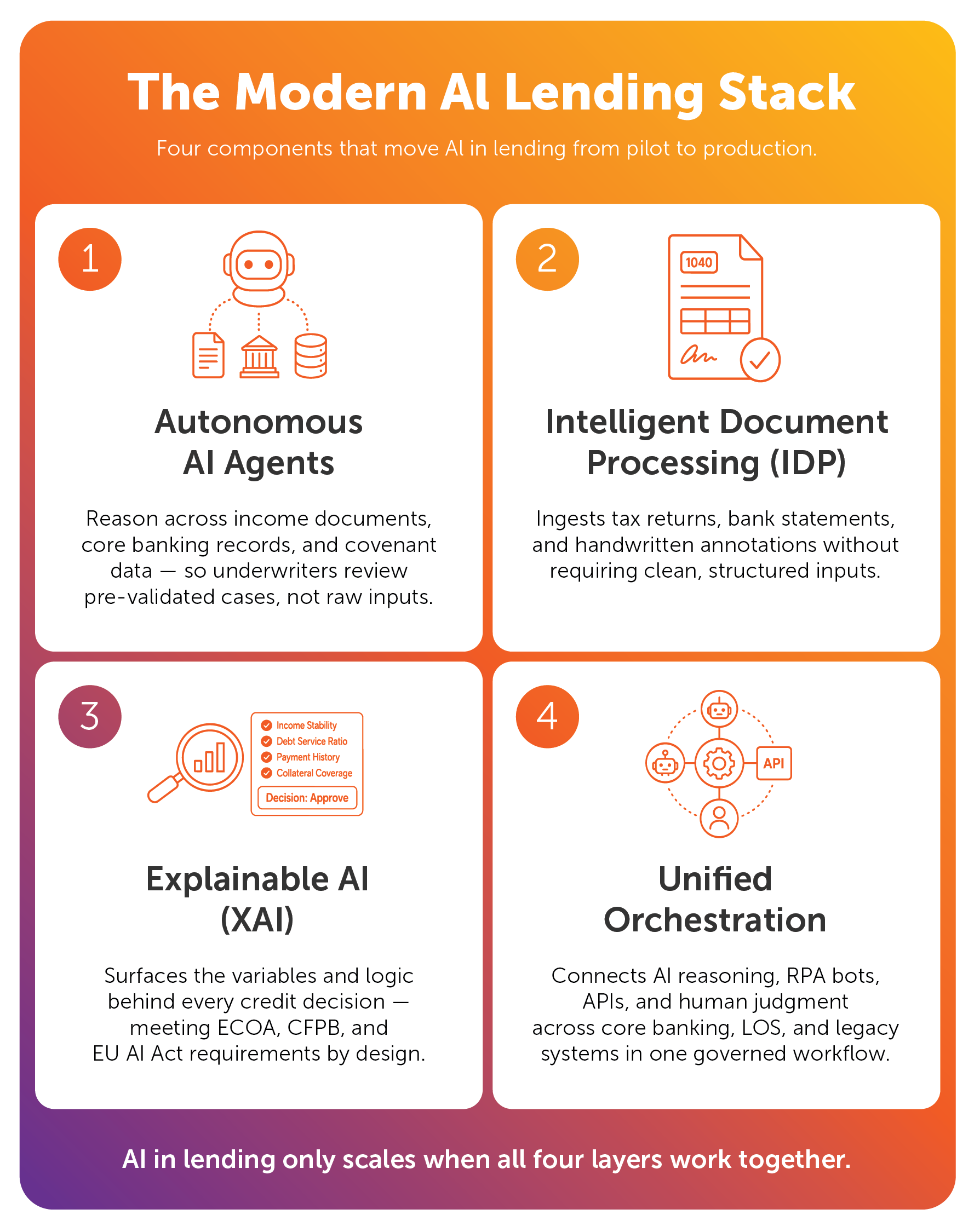

Key components of AI in lending: The modern agentic stack

Autonomous AI agents for complex decision making

AI models in 2026 go beyond simple data classification. Orchestrated agents deployed in commercial lending can cross-reference income documentation against core banking records, flag covenant discrepancies, and weight non-traditional variables.

This allows the underwriter to review a pre-validated case rather than raw inputs, significantly reducing default risk. That same reasoning pattern drives AI in banking efficiency gains across risk, compliance, and servicing wherever complex judgment work follows high-volume data preparation.

AI-powered intelligent document processing (IDP)

The evolution of OCR into intelligent document processing ingestion is one of the most immediate high-value applications of artificial intelligence in lending industry.

Instead of needing clean, structured inputs, modern document automation handles tax returns with handwritten annotations and inconsistently formatted bank transactions. This directly resolves the data quality problems that cause traditional machine learning systems to underperform.

Explainable AI (XAI) for regulatory credit scoring

Regulators now demand that automated systems be transparent. Explainable AI (XAI) surfaces the specific variables and logic paths that produced a credit outcome.

This is essential for maintaining compliance with the Equal Credit Opportunity Act and satisfying CFPB adverse action requirements and EU AI Act obligations. For any institution, and especially when operating under fair lending mandates, XAI is table stakes.

Unified orchestration: Connecting AI to core systems

The single most common reason AI in lending fails to scale is integration. A standard loan workflow requires extracting document data, validating borrowers in the core banking system, retrieving credit files from the LOS, routing approval through the workflow tool, and triggering disbursement. Five systems, likely spanning on-premises, legacy, and cloud environments with different security models and API constraints.

Point solutions fail consistently at enterprises’ hybrid infrastructure, legacy connectivity, and security boundaries that govern where financial data can move.

Automation Anywhere’s APA system is built for this enterprise reality. It starts from the full process mapping every handoff, every system, every actor before deploying intelligent agentic systems into any step.

Orchestration then coordinates the four work actors enterprise lending workflows require: AI reasoning and classification, RPA bots for deterministic structured tasks, APIs for system-to-system data exchange, and humans for final judgment on high-stakes decisions.

Governance operates continuously throughout, with access controls, data masking, and audit logging embedded at every handoff (not added as a separate compliance step that slows throughput). The same orchestration principles extend across AI in business operations wherever regulated workflows require end-to-end auditability.

Key benefits of AI-powered lending

AI lending benefits at a glance

Benefit | Impact on Financial Institutions |

|---|---|

Faster Approvals | Lending processes cut from days to minutes. |

Risk Accuracy | Better credit assessments using alternative data. |

Fraud Prevention | Real-time detection of synthetic identities. |

Financial Inclusion | Expanded approval rates for thin-file borrowers. |

1. Faster loan processing and approval

AI in lending reduces manual touchpoints that create delays across document intake, data extraction, identity verification, initial credit scoring, and exception triage.

Automation Anywhere’s loan underwriting agentic workflows cut processing times by 60%, with one automotive lender reducing approval cycles by 88%, giving institutions the speed to capture high-intent borrowers before competitors respond.

In this video, you will see how leading banks can optimize loan processing with AI agents.

2. Enhanced risk assessment & accuracy

Traditional credit scoring models rely on a constrained variable set. Modern financial organizations analyzes behavioral signals and cash flow patterns.

This broader view produces more accurate credit risk assessments and drives financial inclusion by extending credit to gig workers and first-time borrowers without increasing exposure.

3. Improved fraud detection and real-time mitigation

Fraud detection now operates continuously across the application stream. By identifying synthetic identity patterns and document inconsistencies, AI tools provide proactive fraud prevention, flagging a fraudulent application before disbursement.

In high-volume consumer and SMB lending, the shift from reactive to proactive detection has material impact on loss rates.

4. Scaling commercial lending with agentic automation

Commercial lending has historically resisted automation due to complexity. However, AI technology now handles financial spreading at ingestion extracting data from complex spreads in seconds. This allows the banking sector to shift from periodic reviews to real-time portfolio monitoring.

5. Lower operating costs & increased efficiency

AI could bring gross cost reductions of up to 70% in certain cost categories, with an expected net decrease of 15–20% across banks’ aggregate cost base.

In lending operations, the driver is volume scalability: institutions can process three times more loan applications with AI agents without proportional headcount increases, reducing cost-per-loan structurally rather than incrementally.

6. Enhanced borrower experience & personalization

AI-powered chatbots and virtual assistants deliver 24/7 support and personalized loan guidance, while back-end agents calibrate offers to individual risk profiles versus entire product categories.

Borrowers receive faster decisions, more relevant terms, and real-time status updates throughout the process. The AI in fintech players who built this as a foundation have set the experience benchmark; traditional institutions now have the platform tooling to match it.

The industry-wide impact of AI in lending

The competitive chasm in financial services

Forrester’s 2026 financial services predictions project that AI will automate over a third of manual financial processes such as data processing, reporting, and reconciliation, by end of the year. In a high-interest-rate environment where margin compression is already squeezing traditional lenders, institutions that cannot match the cost-per-loan economics of AI-enabled competitors face a structural disadvantage that compounds with each rate cycle.

Democratizing access through fairer credit scoring

Agentic AI in lending creates a practical mechanism for character-based and cash-flow-based underwriting at scale.

Institutions can extend credit to creditworthy borrowers invisible to traditional scoring models, like gig workers with variable income or first-time borrowers without bureau history, without taking on additional risk. The explainability requirement enforced by XAI ensures that expanded access does not introduce disparate impact.

Transforming Labor: From data entry to agent orchestration

Agentic automation redirects where human expertise is applied across the lending organization.

- Underwriters shift from data gathering to decision-making

- Relationship managers focus on clients rather than file preparation

- Risk officers move from periodic reviews to continuous portfolio oversight

The administrative cognitive load that currently consumes specialized staff is absorbed by agents; the judgment work that requires their expertise is where they spend their time.

AI lending and customer experience

AI-driven personalization in customer engagement

Behavioral data generated throughout a borrower’s relationship, payment patterns, product usage, inquiry timing, and channel preferences give AI models enough signal to shift from reactive service to anticipatory engagement.

An institution can identify when a small business borrower’s cash flow pattern signals an upcoming working capital need and initiate an offer before the borrower searches elsewhere. This proactive posture is what separates AI-driven customer engagement from AI-assisted customer service.

Frictionless journeys: The new standard for customer experience

The benchmark for borrower experience is now set by providers who process applications continuously, eliminate document resubmission cycles, and return decisions in minutes.

For traditional institutions, closing the gap means removing manual handoffs that create friction, in particular status opacity, approval delays, and repetitive document requests.

Orchestrated agentic workflows enable intelligent straight-through processing (STP) that eliminates these touchpoints. This directly improves NPS and long-term retention in a hyper-competitive market where switching costs are falling and digital-first alternatives are only a click away.

AI lending for enterprises (commercial lending)

Automating financial spreading and covenant monitoring

Commercial lending has historically resisted automation because of its complexity: multi-entity financial statements, non-standard document formats, and judgment-intensive analysis that varies by deal structure.

AI-powered IDP now handles complex inputs including multi-entity tax returns, non-standard P&L statements, and handwritten annotations.

Automation Anywhere’s financial services automation flags covenant breaches in real time rather than at the next scheduled review.

Real-time portfolio credit risk management

Annual and quarterly credit reviews are an artifact of manual data-gathering constraints. The shift from periodic assessment to always-on risk monitoring is the structural change agentic automation makes possible in commercial credit.

With continuous data ingestion from core systems, market feeds, and borrower-reported financials, AI agents monitor portfolio risk in real time, detecting early-warning signals, triggering covenant reviews, and escalating exposure changes before they become credit events.

The future of AI in lending: Toward 2030 autonomous finance

The rise of the “personal finance agent”

Analyst predictions describe the emerging agent-to-agent economy: a borrower’s personal AI negotiates with a lender’s AI for optimal rates and terms in real time. For this to function, institutions need machine-readable rate structures, real-time decisioning APIs, and agentic infrastructure capable of responding to AI-initiated queries at scale.

Institutions building AI infrastructure now will be positioned to participate; those that are not will be invisible to AI-represented borrowers.

Hyper-regional risk modeling and quantum readiness

AI models that incorporate hyper-local economic signals — regional employment data, sector-specific revenue patterns, municipal tax base indicators — produce more accurate risk assessments for commercial and community lending than models built on national averages.

As quantum computing matures, it extends that precision to real-time credit decisioning at portfolio scale: running risk simulations in seconds that currently take hours, enabling dynamic pricing and exposure adjustments that static models cannot support.

“Embedded everything”: The invisible loan

The endpoint of AI in lending is a credit decision that requires no separate application: a purchase-order financing offer triggered at the point of B2B transaction, a working capital line activated by an inventory event, a mortgage pre-approval surfaced during a property search.

This embedded finance model does not eliminate underwriting but moves it upstream, automated and invisible to the end user. The orchestration layer connecting lending AI to third-party platforms and contextual data streams is the infrastructure that makes it possible.

Overcoming hurdles in AI implementation

Solving the data quality paradox

Most AI models underperform due to poor input quality. Successful AI adoption requires integrating AI with IDP pipelines that clean and structure data at the point of entry.

Ethical decision making: Bias detection and mitigation

Expanding variable sets in AI credit scoring increases both accuracy and the risk of encoding historical bias. Continuous bias monitoring, disparate impact testing, and explainability requirements must be embedded in the model governance workflow, not as post-deployment compliance review.

Governance: The human-in-the-loop (HITL) security model

Human judgment remains critical. Human-in-the-loop is not a constraint; it is the mechanism that ensures customer trust and regulatory safety.

Automation Anywhere’s APA system produces a complete, examiner-ready audit trail as a byproduct of normal execution.

Conclusion: Winning with an AI-first lending strategy

Leveraging AI agents in banking is transforming the finance industry. The credit lifecycle is being restructured from document intake to capital deployment by agentic AI.

The institutions that will lead through 2030 are implementing a unified agentic platform where workflows are auditable, integrations are governed, and AI decisions connect to systems of record.

Automation Anywhere’s APA system provides the proven infrastructure for that operating model, at the scale and compliance standard that enterprise financial institutions require.

FAQ: Navigating AI-powered lending in 2026

How does AI in lending impact the accuracy of credit risk?

Machine learning models analyze a broader set of variables, including cash flow behavior and sector-specific risk signals. This results in more granular and predictive credit assessments than traditional methods.

How can banks ensure regulatory compliance when they adopt AI?

Institutions must utilize Explainable AI (XAI) to provide clear "reason codes" for credit decisions, ensuring they meet the requirements of the Equal Credit Opportunity Act.

What is the impact of AI on the lending lifecycle?

AI reduces manual intervention across the lending lifecycle from loan origination to ongoing monitoring, allowing staff to focus on customer engagement and complex decision making.

What are the first steps for financial institutions starting an AI implementation?

The highest-return starting points are high-volume, document-intensive processes where data quality and processing speed are primary constraints, like loan origination, income verification, and fraud detection. Leverage a platform that connects to your existing LOS and core banking systems, with native governance and audit infrastructure.

How does commercial lending benefit from artificial intelligence compared to consumer?

Commercial lending presents a larger AI opportunity on a per-transaction basis deal complexity, document variation, risk variables, and manual burden compound to limit volume and slow cycle times. AI-powered IDP, financial spreading automation, and covenant monitoring address the bottlenecks: analysis time, covenant review frequency, and multi-entity data aggregation.

Stay up to date:

Try

For Students & Developers

Start automating instantly with FREE access to full-featured automation with Cloud Community Edition.