- Login

- Search

- Contact Us

-

Have a question? Our team is here to help guide you on your automation journey.

-

Explore support plans designed to match your business requirements.

-

How can we help you?

-

English

Close

- Resources

Featured

Named a 2026 Gartner® Magic Quadrant™ Leader for RPA.Recognized as a Leader for the Eighth Year in a Row Download report Download report

Named a 2026 Gartner® Magic Quadrant™ Leader for RPA.Recognized as a Leader for the Eighth Year in a Row Download report Download report

- The role of AI in the payments industry

- Key takeaways

- Beyond fraud detection: The shift to lifecycle AI in payments

- Why payments are a state and exception management problem

- Where AI and machine learning create value across the payment lifecycle

- High-value use cases for AI in payments

- Common challenges when adopting AI in payments

- How to introduce AI into payment operations

- The 2026 landscape of artificial intelligence in payments industry

- How Automation Anywhere’s P2P solution makes payments more efficient

- AI and payments industry FAQs

- Can AI really reduce false declines?

- How does AI help with cash flow?

- How does Automation Anywhere support human-in-the-loop review for sensitive payment decisions?

- What guardrails help ensure AI-driven payment actions remain auditable and compliant?

- What are the latest trends in AI-powered payment gateways?

- Can AI improve the security of online transactions?

The role of AI in the payments industry

The role of artificial intelligence (AI) in the payments industry centers on managing complex operational workflows that occur after the initial transaction. In the modern enterprise, digital payments have transitioned from a back-office utility to a primary driver of payment processing efficiency. However, as transaction volumes surge, the operational complexity surrounding those transactions has grown exponentially.

Payments have become one of the most operationally demanding functions in modern enterprises. The challenge is no longer just the sheer volume of payment processing; it is the downstream work created when payments fail, stall, partially settle, or reverse after initiation.

A single failed authorization can trigger a cascade of events: intelligent retries, customer outreach, reconciliation checks, and potential disputes. At scale, these downstream workflows consume more operational effort than the initial transaction itself.

This guide explores the evolving role of artificial intelligence in managing the end-to-end payment lifecycle to reduce costs and improve customer satisfaction.

Key takeaways

Lifecycle orchestration: AI in payments extends beyond fraud detection to manage retries, reconciliation, and dispute resolution.

Exception management: Intelligent models parse ambiguous payment states, reducing manual intervention in soft declines and network timeouts.

Financial accuracy: Automated matching and ledger alignment ensure continuous reconciliation, reducing month-end audit risks.

Agentic automation: Agentic process automation persists across the payment lifecycle, maintaining state awareness until financial finality.

Beyond fraud detection: The shift to lifecycle AI in payments

Most discussions of AI in payments focus on a narrow set of use cases: fraud detection, authorization optimization, and approval rate improvement. These are undoubtedly important; however, they address only the moment of transaction initiation.

They do not address the operational burden that follows when transactions move into ambiguous or exception states. To truly streamline operations, the finance team must look toward AI systems that manage the "state" of a payment over time.

Identifying the true friction in payment operations

The true friction in payment operations stems from a lack of visibility and the manual handling of complex payment processes. This includes:

- Failed and declined transactions: These require sophisticated evaluation, retry logic, and empathetic customer communication to avoid churn.

- Reconciliation mismatches: Discrepancies across gateways, payment providers, banks, and internal ledgers often require manual data entry to resolve.

- Disputes and chargebacks: These processes unfold over weeks, requiring strict adherence to deadlines and evidence requirements.

- Manual coordination: This occurs in the constant back-and-forth between payments operations, treasury, and customer support.

These downstream workflows consume disproportionate resources and introduce compounding financial and regulatory compliance risk as volume scales.

A payment is not a single event, but a stateful process that unfolds over time. Authorization is the beginning, not the end. Financial finality requires settlement, reconciliation, and sometimes dispute resolution. Each stage can introduce exceptions that demand structured follow-through by AI models.

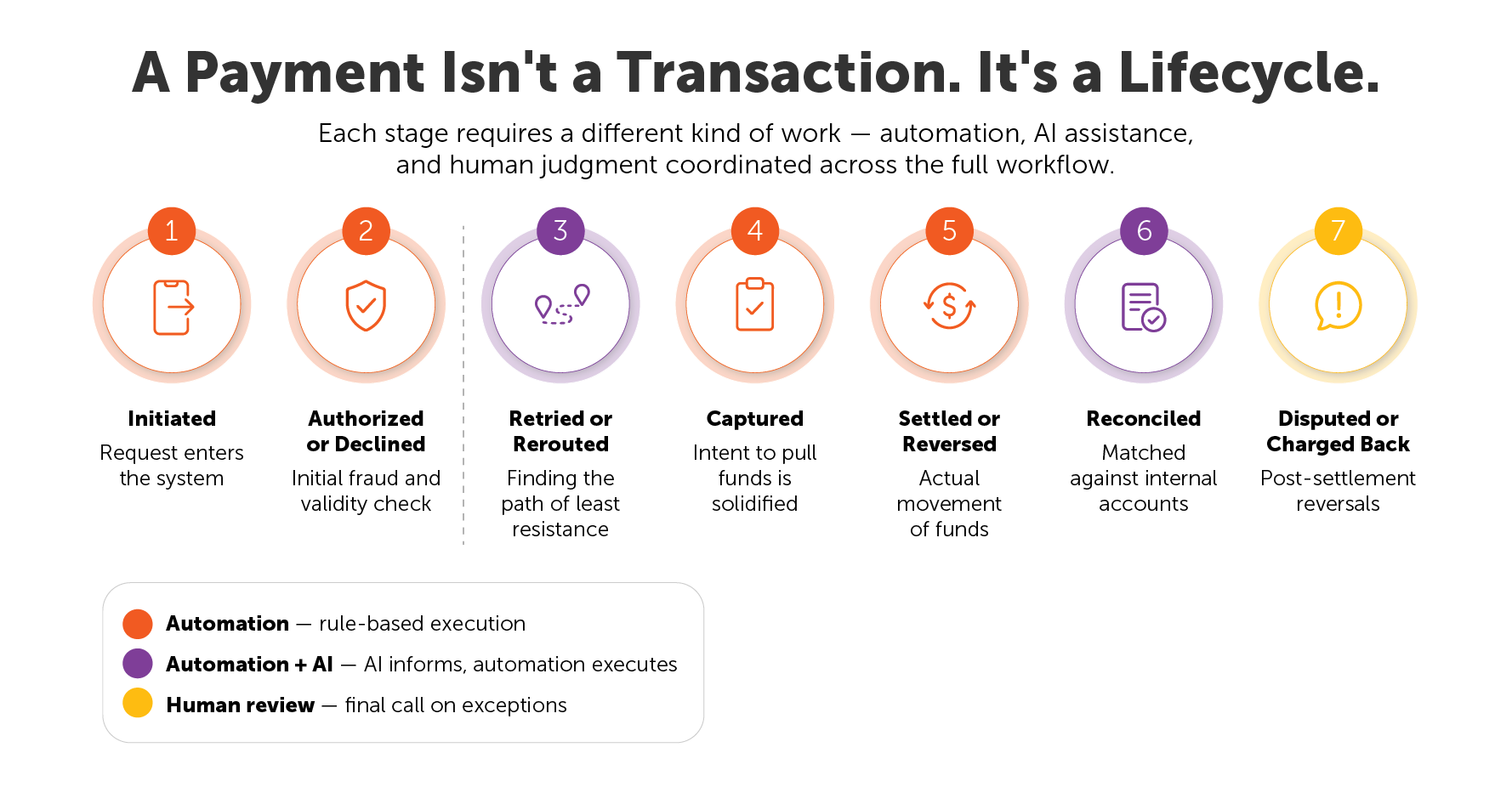

Why payments are a state and exception management problem

Most legacy payment systems treat a payment as a discrete event with a binary outcome: approved or declined. In reality, digital payments are processes that evolve, and their outcomes can change after the initial authorization attempt. Understanding this "statefulness" is critical for implementing AI effectively.

The asynchronous nature of digital payments

A typical payment moves through multiple states, often asynchronously:

- Initiated: The request enters the system.

- Authorized or declined: The initial check against fraudulent transactions.

- Retried or rerouted: Using payment routing to find the path of least resistance.

- Captured: The intent to pull funds is solidified.

- Settled or reversed: The actual movement of financial data and funds.

- Reconciled: Matching the transaction against internal accounts.

- Disputed or charged back: Post-settlement reversals.

Each state transition can occur across systems owned by different parties: gateways, processors, card networks, and issuing banks. When these systems don't talk to each other, human error in data entry and reconciliation becomes inevitable.

Payment Lifecycle Stage | Traditional Approach | AI-Driven Approach |

|---|---|---|

Decline Handling | Blind retries based on static rules | Context-aware retries optimizing approval rates |

Reconciliation | Manual batch processing at month-end | Continuous, automated ledger matching |

Dispute Management | Reactive, manual evidence gathering | Predictive modeling and automated submission |

Distinguishing exceptions from hard failures

Most payment failures are not "hard" failures (like an invalid account). They are exceptions requiring interpretation:

- Soft declines: Temporary issues that may succeed on a secondary retry.

- Network timeouts: Ambiguous outcomes where the state is unknown.

- Partial settlements: Requiring granular transaction data to reconcile.

- Ledger mismatches: Inconsistencies between payment providers and internal records.

Traditional rules engines assume linear, deterministic flows. They break down when outcomes are ambiguous. Machine learning and AI tools are required to navigate this ambiguity, using predictive analytics to decide the next step.

Where AI and machine learning create value across the payment lifecycle

AI in the payments industry creates value not by optimizing a single stage, but by reducing friction across the full lifecycle. This is where machine learning models and generative AI tools provide the most significant ROI.

Decline handling and revenue recovery

Not all declines are final. Soft declines, issuer timeouts, and transient network errors represent recoverable revenue. But distinguishing recoverable failures from hard declines requires contextual awareness.

Blind retries increase fees and frustrate individual customers. Abandoned declines leave revenue on the table. AI tools can evaluate decline codes, historical issuer behavior, and transaction data to determine whether, when, and how to retry. This directly impacts authorization rates and reduces involuntary churn, which is vital for maintaining customer experience.

Settlement, capture, and financial data integrity

Settlement exceptions often surface after customer-facing systems assume success. When settlement fails or is delayed, downstream correction becomes costly. AI systems can monitor settlement files and processor confirmations in near real time, identifying anomalies before they propagate into ledger discrepancies. Early detection reduces month-end reconciliation pressure and prevents compounding financial loss.

Reconciliation, ledger alignment, and accounts payable

Reconciliation is one of the highest-friction stages in global payments. Data arrives on different timelines and in varying formats. Small mismatches escalate into larger discrepancies if left unresolved.

AI applications using natural language processing (NLP) can match records, flag inconsistencies, and even automate invoice processing. Instead of periodic batch reconciliation, the finance team gains continuous ledger alignment, reducing audit risk and improving cash flow visibility. In accounts payable, this ensures that vendors are paid accurately and on time, maintaining healthy supplier relationships.

Disputes and chargeback lifecycle management

Disputes represent a parallel lifecycle that can reverse settled payments weeks later. Each dispute has strict evidence requirements. AI in payments can track disputes from initiation, gather relevant payment data, and ensure timely responses. By reducing false positives in the dispute process, companies can reduce risk and protect their revenue.

High-value use cases for AI in payments

The following use cases illustrate how AI technologies operate in practice, going beyond what embedded gateway features can accomplish.

Intelligent retry and fallback orchestration

AI models evaluate decline codes, issuer patterns, timing windows, and customer lifetime value. They may:

- Delay a retry to align with issuer behavior.

- Route to a secondary gateway via advanced payment routing.

- Switch payment methods (e.g., from card to ACH).

- Escalate high-value transactions for human judgment.

The outcome is higher recovery rates, fewer wasted retries, and a marked improvement in payment processing efficiency.

Exception triage and investigation automation

Transactions in ambiguous states require investigation. AI systems gather context from payment logs, ERP entries, and financial data. They classify which exceptions can be resolved automatically and which require a financial professional. This reduces investigation queues and ensures consistent handling of complex payment processes.

Reconciliation and invoice processing automation

AI agents match records across sources. When discrepancies arise, they initiate actions such as requesting missing files or flagging breaks. In accounts payable, AI can automate the ingestion of invoices, reducing human error and ensuring that data entry is handled with 100% accuracy.

In this video you will see how accounts payable teams spend hours chasing missing PO documents, managing vendor communications, and manually processing approvals.

Dispute lifecycle and fraud prevention

Machine learning tools track disputes end-to-end. By analyzing training data from past disputes, these models can predict the likelihood of winning a case and automate the evidence-gathering process. This is a core component of modern fraud detection and prevention strategies.

Common challenges when adopting AI in payments

Payments leaders see the opportunity in AI but often struggle with structural barriers. Understanding these challenges is key to successful implementation.

Fragmented data and asynchronous systems

No single system has a complete view of the payment state, as payment data is fragmented across systems and parties. Effective AI in payments requires an orchestration layer that assembles context across sources, from gateways to bank portals.

Financial accuracy, auditability, and regulatory compliance

Payments automation must preserve financial integrity, and every retry, reversal, and adjustment must be traceable. Regulators increasingly demand explainability in how AI models make decisions. AI systems must log decisions and tie them to explicit policies to comply with the regulatory landscape.

Legacy infrastructure and real-time demands

Many payment systems still rely on manual processes like batch processing and legacy APIs. AI agents must be capable of operating across modern APIs, flat files, and human workflows simultaneously. Pure API-driven automation is often not possible in legacy payment environments.

Human oversight and decision making

Payment decisions frequently require human judgment, especially for high-value exceptions or fraud detection cases that might result in discriminatory outcomes. AI technologies must support structured escalation rather than purely autonomous decision-making.

How to introduce AI into payment operations

Applying AI to payments is not about replacing your stack; it’s about automating the operational work surrounding money movement.

1. Start with post-authorization workflows

Authorization and fraud detection are already heavily optimized by gateways. Begin with post-authorization workflows — like retry orchestration and reconciliation — where the operational impact is high, but the integration risk is lower.

2. Map payment states and define ownership

It is critical to define payment states — initiated, authorized, captured, settled — and document what triggers transitions. Each state needs an owner, whether it is an AI agent or a member of the finance team.

3. Encode retry and routing policies explicitly

AI agents must operate within clearly defined rules. Explicit policy encoding is critical for trust and regulatory compliance. AI cannot enforce policies that exist only in "tribal knowledge."

4. Establish human-in-the-loop controls

For high-risk scenarios, such as disputed charges or reconciliation breaks above a certain threshold, AI should surface context and recommended actions to a human reviewer. This ensures that potential risks are managed while still benefiting from AI speed.

The 2026 landscape of artificial intelligence in payments industry

By 2026, payment environments will be shaped by widespread adoption of ISO 20022 and the expansion of real-time payments.

Richer data and ISO 20022

The transition to ISO 20022 will significantly increase the richness of transaction data. This creates a massive opportunity for AI systems to make more context-aware decisions about routing and reconciliation. However, it also increases the burden on systems to process this data at scale.

AI-initiated spend and machine-to-machine commerce

AI is no longer just analyzing payments; it is beginning to initiate them. Enterprises are deploying agents to automate procurement and treasury optimization. This shifts the challenge from managing human-initiated transactions to governing AI-initiated financial activity.

Compressed decision windows in real-time payments

As real-time payments networks expand, the tolerance for delayed reconciliation shrinks. Fraud detection and prevention must occur in near real time. AI systems must react to events as they occur, not hours or days later, to prevent financial loss.

Evolving regulations and explainability

As AI becomes embedded in financial workflows, the regulatory landscape will intensify. Supervisory bodies will focus on traceability. Payment automation cannot rely on "black box" logic. Systems must demonstrate why a transaction was escalated or a retry attempted.

How Automation Anywhere’s P2P solution makes payments more efficient

Automation Anywhere automates payment operations, not payment processing itself. It does not replace gateways, processors, fraud engines, or card networks. Its Agentic Solution for Procure-to-Pay has a deep understanding of each step of the end-to-end payment lifecycle and the intent behind each operational step, and it leverages AI agents to execute and coordinate retries, reconciliation, disputes, and cross-team workflows.

Its AI agents persist across a payment’s lifecycle, tracking state changes and responding to events like soft declines or settlement delays. They operate across fragmented infrastructure via APIs, RPA, and file-based integrations, connecting gateways, processors, ERP systems, treasury platforms, and support tools.

Governance is enforced at the process level. Every retry, routing decision, escalation, and adjustment is logged with context, creating an audit trail that finance, compliance, and external auditors require. AI agents handle interpretation-heavy tasks like classifying exceptions, summarizing transaction histories, and recommending next actions. Automation Anywhere’s Procure-to-Pay solution manages routing, execution, and human-in-the-loop oversight for sensitive decisions.

AI and payments industry FAQs

Can AI really reduce false declines?

Yes. By using predictive analytics and analyzing training data from successful legitimate transactions, AI models can identify when a decline is likely a "soft" error, allowing for a strategic retry that saves the sale and improves customer experience.

How does AI help with cash flow?

AI helps improve cash flow management by analyzing payment patterns, predicting inflows and outflows, and identifying risks such as late payments, failed transactions, or liquidity gaps. AI agents can also automate collections follow-up, reconcile receivables faster, and provide finance teams with real-time visibility into working capital and cash positions.

How does Automation Anywhere support human-in-the-loop review for sensitive payment decisions?

Automation Co-Pilot provides an interface for payments and finance teams to review exceptions, approve retry strategies, or evaluate dispute responses. Agents surface context and recommendations, while humans retain decision authority for high-risk cases.

What guardrails help ensure AI-driven payment actions remain auditable and compliant?

APA embeds governance at the process level. Every action is logged with context, policy reference, and timestamp. Retry limits, routing constraints, and escalation triggers are encoded explicitly. This ensures traceability for finance, compliance, and external auditors while maintaining operational efficiency.

What are the latest trends in AI-powered payment gateways?

The payments landscape in the United States has undergone a massive transformation, moving far beyond simple transaction processing. AI is no longer just a backend optimization tool; it is actively rewriting how transactions are initiated, routed, and secured.

Can AI improve the security of online transactions?

Yes. AI is already improving the security of online transactions, particularly by helping financial institutions and merchants detect fraud faster and respond more intelligently. However, it's most effective when combined with established security measures rather than used on its own.

AI in payments is about orchestrating the full lifecycle of money movement. Request a demo to see how organizations can reduce exception cost, improve recovery rates, and maintain the financial integrity required in modern payment ecosystems by applying agentic process automation.

Stay up to date:

Try

For Students & Developers

Start automating instantly with FREE access to full-featured automation with Cloud Community Edition.